With a little left to go in the first quarter, I’ve published almost 40 blog posts, even with work travel taking priority over the last few weeks. My previous high for a year is just over 50. I’m on pace to potentially triple my output.

I heard two things on podcasts yesterday that reminded me not to let these last few weeks determine how I keep building the habit.

Seth Godin said:

“I wrote this morning because it was Thursday, not because I planned to publish the best thing I’ve ever written.”

What a powerful statement – especially for those who are just getting started or afraid to publish anything.

The first part is so important. There’s something about knowing I have to meet the keyboard every morning that makes me more observant, more present, and more curious.

More and more, I realize it pulls me out of a passive consumption mode into a thinking one and eventually into a creation mode. That’s something worth working hard on.

Writing is a tool to reach beyond observation until you connect concepts and step into actionable territory. That actionable territory in my world is helping companies or discovering an investible thesis.

Another good nugget from yesterday came from Shaan Puri, “We write so someone can binge our content and feel like they know us.”

Usually, people find my writing before or after meeting with me. I’m not trying to write for vitality, so the first time someone interacts with the blog is because we’re potential partners at some point.

For the first time, not writing made me unsettled. I have a list of topics I want to write about, and these were good reminders not to let a few inconsistent weeks be the downfall of what I started in January.

So, what’s coming up? Here are a few things I’ll post about soon:

Speed + Focus = Intensity

The Professionalization of the Trades

Victory is spelled Survival

Repetition Doesn’t Spoil the Prayer

Intelligence Breeds Overconfidence

Opposites Create Opportunities

Thank you for following along, even when most posts are not the best thing I’ve ever written.

The energy transition requires more skilled labor – stop me if you’ve heard this one before.

In a conversation often confined to the US, energy transition related job opportunities are coming to the UK and EU, too. A new report by Bain estimates that over 1 million jobs will be created by 2030 due to the energy transition, and another 4 million roles will need significant reskilling.

Unsurprisingly, the vehicle manufacturing industry will drive more gross and net role losses than any other sector, as low-emission vehicles require less labor to manufacture and service than their internal combustion engine counterparts.

The home heating and electrician sectors are due for a boom. Bain estimates up to 170,000 new heat pump installer roles will be required, outweighing the 60,000 installation jobs lost as gas boilers phase out.

Europe will also undergo a continent-wide AC installation movement as temperatures rise in areas where AC was a novelty due to temperate climates.

However, most of the transition will require a new set of skills. Only about a third of legacy roles will have a clear replacement in the net-zero transition. There may be overlapping skill sets between legacy and green roles, but most will require some retraining.

Rightfully, some companies remain hesitant to retrain their workforce for jobs they aren’t sure will exist in a few years. The energy transition has just started, and some new technologies might not exist in a decade. Long-term demand will solidify support for training a new workforce in most sectors.

We can bet that if the UK has a labor problem of this size, the US opportunity is at least 2- 3 times as large.

Labor shortages will continue to grow as our population ages, and people seek desk-based jobs due to economic mobility. The latter might be a mistake. The reward for supplying labor to the energy transition will be enormous.

Can I successfully connect my kids’ TV habits to Napoleon and then turn it into a commentary on climate? Let’s give it a shot.

My son Ian loves a Netflix series called “Alphablocks” and its math-based spinoff “Numberblocks.” In both, the characters tell a story – supported by song and dance – to teach foundational concepts.

He learns 3×3=9 or that “ph” makes the “f” sound in words because he remembers the episode’s story. He also learns a few songs I’ll hear on repeat for months on end.

Steve Jobs famously said, “1,000 songs in your pocket.” It certainly sounds much better than “x” GBs of storage for music.

Churchill was a surprisingly lousy politician. But, he was a prolific writer and speaker. He once wrote to a colleague:

Each year it is necessary for a modern British Government to place some large issue or measure before the country, or to be engaged in some struggle which holds the public mind.

He understood the power of controlling the story.

Napoleon knew that the narrative coming from the battlefield shaped the collective mood of France’s revolution. He managed every detail of information flowing back to Paris and even embellished it for his wife to ensure the story stayed consistent.

He displayed an extraordinary ability to present terrible news as merely bad, bad news as unwelcome but acceptable, acceptable news as good, and good news as a triumph.

All of them realize(d) that the best story wins. (we did it!)

Morgan Housel popularized this idea in his new book Same as Ever, but he initially shared the insight in 2016 on an episode of The Knowledge Project.

Almost every winning campaign in recent history is devoid of facts and instead embraces a feeling.

Think Different: encouraged everyone to push the boundaries

Just Do It: inspired millions to embrace their inner athlete

Various political examples that I won’t get into. This isn’t a politics blog

Sometimes, I wonder if the climate movement is winning this battle.

Talented people pour into climate technology companies daily because they believe in the story that adds meaning to their work. There’s 10x more capital focused on funding companies in climate than at the peak of Climate 1.0. More successful startups are raising money and gaining real traction than ever before.

At the same time, I see headlines celebrating the decline of electric vehicles while the market grows 30% a year. Or, I read about major banks pulling out of ESG movements, all while their investments in sustainability continue to grow.

Because we’re a community of (mostly) logical people, we see the problem and an investment opportunity of the lifetime then back it up with facts. However, the stories that unleash the forces of the masses don’t require logic or facts.

Ironically, it’s the opposite. The people who can throw facts, self-awareness, and consciousness to the wind tell the best stories. That makes selling others easier. Sometimes that’s good, sometimes it’s terrible.

An uncomfortable truth is that bad ideas with strong support will almost always do better than good ideas with poor support. Our collective hope is based on the belief that these movements eventually require a “there” there, but a story goes a long way.

Doomerism, despite being the preferred method of some, also doesn’t work. Several studies, including a recent one published in Science Advances, found that if everyone thinks we’re doomed, they’ll go about their normal routines anyway. The doom and gloom demoralizes the public into inaction despite getting much of the attention.

The rule trickles all the way down to companies, too Great stories raise money (sometimes too easily), great stories sell products, and great stories attract great people.

Movements are born from great stories, and the climate movement could use more storytellers. But, of course, storytelling is a slippery slope if not paired with copious amounts of intellectual honesty and humility, something the world could use a lot more of.

Do you ever feel bombarded by the same story over and over again? Lately, I can’t dodge stories highlighting insurance’s growing costs due to climate change.

In his annual letter, Warren Buffet started sounding the alarm on wildfires and their risk to investment in utilities that were once considered safe bets. He wrote, “Certain utilities might no longer attract the savings of American citizens,” as Berkshire Hathaway faces over $8B in claims from fires in Oregon and California.

These claims lead to rising insurance rates and rightfully require significant investments into disaster mitigation efforts. It’s a catch-22, utilities need the insurance and must prevent disasters where they can because the humanitarian tolls are too great. However, the costs are large and raising rates to cover them is an uphill battle.

Yet, abandoning utilities as an investment class would be disastrous. We need them to maintain the aging infrastructure we already have. A lack of investment into utilities will also hinder their ability to build the infrastructure we so desperately need as renewables further penetrate the grid.

Speaking of renewables, insurance has grown into one of the major headwinds hindering the deployment of utility-scale solar in the US. These projects need guarantees for up to 40 years, and recent hailstorms and floods drove premiums to unprecedented heights.

A few extra percentage points make all the difference in a sector with razor-thin profit margins.

These businesses aren’t the only ones facing rising insurance premiums. Consumers are getting crushed, too.

Some insurance companies have left states like California and Florida altogether. This departure creates a void of competition, which compounds as the remaining insurers can and must raise prices to account for the risks they are taking.

Insurance will define the housing bubble in these states, not interest rates.

So, what do we do? Unfortunately, this feels like one of those situations where there’s not much we can do, and I hope I’m wrong. Extreme weather will likely continue, and those who insure assets with higher risk will command higher prices.

We’ve seen many startups tackling the consumer space with new business models, and I’m hopeful they’ll succeed. But, scale and capital are insurance’s advantage so starting them from scratch is hard.

New tools for existing insurance firms exist as well.

Insurance companies have more access to data and simulations than ever, too. But the thing is, they’re already good at predicting disaster – the hard part is paying for them.

That’s one thing innovation won’t solve overnight. We can mitigate the risks caused by climate change, but we can’t eliminate them; even the mitigation will take time.

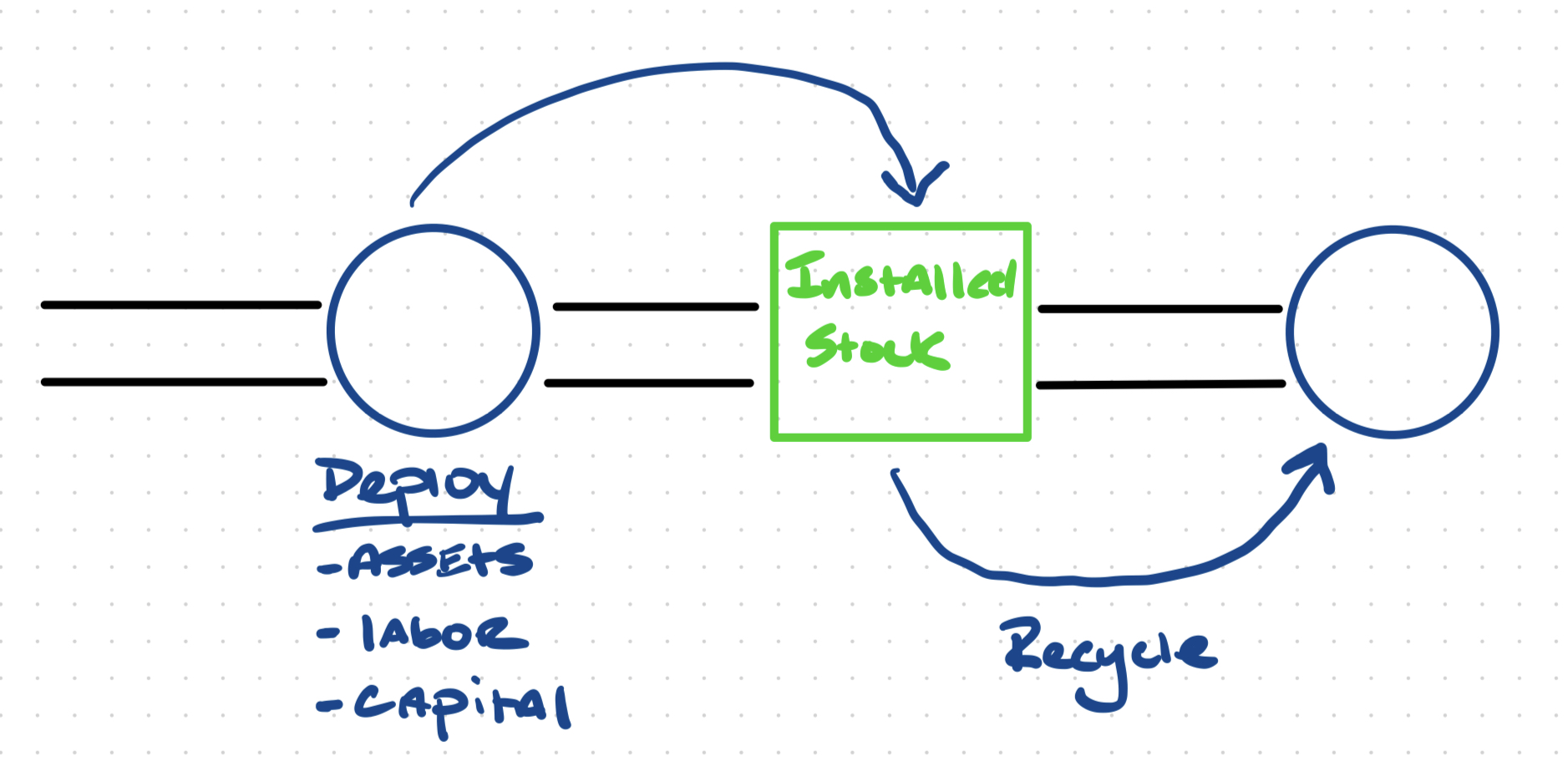

The energy transition is full of deployment, recycling, and retraining. Playing these trends effectively can be a key to success.

Investors like Bill Gurley and Josh Wolfe cite Thinking in Systems as one of the most impactful books they’ve ever read.

A key concept from that book, and one that I’ve been thinking more about lately, centers on the stocks and flows of a given system. The energy transition is full of examples.

New assets like solar, batteries, data centers, and EVs create massive “in-flows” as we deploy those assets at record rates.

The stock consists of existing generation, transmission, and the labor servicing them.

And, soon, we’ll see outflows of assets that are being retired or recycled.

Matching your business to the appropriate part of this cycle can create an unexpected edge. Mismatching can result in disaster or at least slow growth. For example, the environment remains challenging for startups seeking to build O&M solutions for asset categories with small installed bases.

Flow

The easiest way to think of flow in our context is to tie it to deployment to grow the stock and retirement or recycling to shrink it.

The asset side of the energy transition remains firmly in the deployment phase thanks to solar, storage, and EVs. Boosted by AI, data centers will also stay in the deployment phase for the next several years. Startups indexed to flow should quickly achieve product-market fit if their solution solves critical pain points.

Recycling is another great example of flow. Recently, firms within the circular economy have gained more traction as the stock of certain goods needs to flow into new uses. We’ve seen firms like Redwood Materials and Solarcycle have success in batteries and solar, respectively.

Stock

Unlike flow, stock is more intuitive to understand. It is the installed base of a given market’s assets, labor pool, or existing population. So long as in flows are greater than out flows, stock goes up. The magnitude of the difference determines the velocity of stock growth.

As startups grow and mature, investors increasingly consider metrics like gross and net dollar retention to evaluate the health of a company. In addition to continually solving deployment issues, one great way to grow these numbers is by creating value attached to a growing stock.

Over the last year, we’ve seen several companies indexed to the existing stock of energy assets prove to be extremely sticky. These firms usually fall into the categories of operations and maintenance, analytics, and systems of record.

Firms that service/manage EV chargers, provide portfolio-level views of solar and storage, or keep records of installed infrastructure continue to grow in importance.

Stock Meets Flow

The graph above is an oversimplified version of stocks and flows. In reality, many stocks and flows interact with one another. Retraining labor for new industries highlights this example.

There are three ways to solve this problem using the stock and flow framework.

Create more flow by training new workers to grow the installed labor base. Population growth eventually limits this flow’s velocity as only so many workers enter the market at a given time.

Improve productivity of the installed base of labor. Do more with less. This one has worked in industries where software created exponential efficiency gains.

Steal from other tangential labor pools. We could, and are trying, outflow labor from incumbent industries and re-direct it to create an inflow of labor to next-gen energy transition industries. The graph above illustrates this.

So far, #2 has proved the most successful. But, we continually see new solutions arise for #1, and new policies like the IRA could accelerate #3.

Stocks and flows are not mutually exclusive. The companies that index themselves to both at the right time do incredibly well.

Software can accelerate deployment / flow and thus revenue, THEN enable new revenue or reduce costs with solutions for a large stock of assets. In that case, you have created an end-to-end solution for some of the most important customers in the world.

Every social media post looks the same now. Every tweet, thread, or LinkedIn post holds the same formula for engagement because we solved the problem of each algorithm.

Add a post to the algorithm, auto-tune to reach the masses, and end up with a relentless march toward mediocrity. Now, everyone competes for the same attention in the same format on the same platforms.

We see this everywhere. It’s not only social media that’s guilty of the crime. Most websites look the same, and a lot of software takes queues from Notion.

TPG co-founder Jim Coulter put this problem in the context of private equity by saying, “You raise money on doing the same thing (that you’ve done, and most others are doing), but it’s a terrible way to invest and thrive as a firm.”

We gravitate to the middle because it’s where returns (money, attention from others) appear easiest to find. It’s also where there’s less work, and humans are predisposed to doing what’s easy.

If I am to avoid doing unusual things, it becomes difficult to see what chance I have to be more than an average person. – Winston Churchill

What we miss, however, is that someone always shows up with something “everyone” says will not work, but it does, and the game resets. The BIG returns and money go to the person (or businesses) that reset the game.

The secret is that the edges, where there’s less competition, is ultimately an easier place to win.

The irony is that if we’re successful on the edge, our niche becomes the middle, and competition increases. Competition creates healthy markets but makes staying ahead harder as a company or individual.

Steve Schwarzman famously notes that Blackstone always looks to innovate because the cost of capital eventually becomes a race to the bottom in any market where returns are clearly apparent. Replace “bottom” with “middle,” and you have the current state of many things today.

Failure has never scared me. We can’t improve without taking risks. Mediocrity scares the hell out of me – being average often means we didn’t do anything different or push the boundaries.

Let’s keep pushing those boundaries, and doing things differently.

Once companies cross $10M in revenue or ARR, the right product leader becomes a secret weapon for the next stage.

If the first $10M relies on speed and execution. The next $100M adds strategy, operations, and coordination. The right product leader adds all three.

After $10M in revenue, the next leap is from product to complete platform and growing into the de facto solution for your customer. Instead of solely building and selling a product, we need to consider increasing wallet share among our existing customers (white space) and/or expanding to new ones altogether (green space).

The first $10M centers on repeated execution. After $10M, we intuitively increase the importance of new capabilities in finance and operations. But, the product organization often gets overlooked because it’s usually already “good enough.” Someone is coordinating the roadmap, so the potential hole isn’t glaring yet.

The teams that grow most effortlessly have an advantage within their product function. They’re building what the customer wants and doing so quickly. Those that don’t will eventually lose to competitors or have an R&D function that becomes a drain on the P&L, sometimes unknowingly.

So, what’s the difference between good and great. And what do you look for?

Great product leaders tend to always have three traits in common:

They are customer-obsessed, not technology-obsessed. Building the right product for the customer is more important than leveraging the latest and greatest technology. If the latter solves the former, great. If not, solving the customer’s needs comes first.

They understand the entire business and create cross-functional buy-in. The sales team loves them because they take the input and turn it into solutions for the customer. The marketing team loves them because they can explain solutions in lay terms and understand what creates the right to win. Finance loves them because they’re P&L obsessed. The entire organization loves them because they’re accountable.

They balance the long-term with the short-term. The sales team needs to close deals today, but if the product isn’t great in 3 years, they’ll have nothing to sell. Building great products requires a balance of this understanding. They’re laying the groundwork for the future without sacrificing revenue and the P&L today.

It’s not enough to know the desired traits of a product leader. We also have to think about how good/bad shows up in the metrics. Since the product team is usually in place at $10M ARR, recognizing a weak product organization can take longer to show up in the numbers.

The boiling frog analogy applies here. The pain point will grow slowly over time. By the time you realize it, you’re cooked, and a significant change is needed. The solutions are often painful and expensive, both financially and culturally.

A few early signs of poor product leadership include:

Sprint points (what the engineering team is working on) begin skewing too far in the direction of solving bugs, QA, customization, and non-revenue generating / not scalable issues. I like to think of new feature development as leading indicators of future revenues. It will show up in sales if they’re not being worked on.

The margins of implementation and customer success begin to drag. In the former, it’s usually an indication of a high level of customization if you’re pricing the service correctly. If margins within CS are poor or inconsistent, it’s often due to a solution that can be solved with software.

Win/loss ratios begin to shift due to incomplete feature sets. If customers consistently pick other solutions because of missing features, the product organization isn’t effectively strategizing for the future.

The cost of bad product leadership compounds. Eventually, the sales pipeline begins to stall as competition increases and the team burdens the cost section of the P&L outside their own team. Generating less revenue with a higher cost structure is a recipe for disaster.

Product managers catch a lot of grief, and some of them rightfully so. The “CEO” of the product monicker, popularized by Ben Horowitz, inflated a lot of egos.

But, the right product leader creates a competitive advantage. The right product leader views themselves as a servant to the other parts of the company, helping each do their job better. Find yourself the right product leader, and the entire organization will feel the effects.

AI, frontier tech, and hardware grab the headlines while services fly under the radar.

The genesis of Silicon Valley and the lure that it holds started in hardware. But you wouldn’t know it today as the venture capital industry has increasingly turned to software for returns.

It’s hard to blame them. Software produces the biggest returns and scales more easily than other business models. Buoyed by this upstream focus, private equity also turned to software as the industry matured and “ate the world.”

Kyle Harrison recently argued in this well-written piece that hardware could be on its way back to popularity in Silicon Valley. He correctly warned that venture capital runs the risk of treating hardware like software, which could be a disaster.

Nonetheless, some venture investors have turned their attention to hardware because it’s:

a) viewed as the next big thing as a result of on-shoring, the energy transition, and space and;

b) the belief that software will become more accessible due to AI, and thus, competition will grow exponentially over the next decade.

The latter could come to fruition. But, and I can’t overstate this enough, building the software is only ~25% of the battle. Once software is built, that product needs to be sold and implemented. As a company grows, hiring, strategy, and execution all increase in importance. If everyone can build software, domain expertise will become the differentiator.

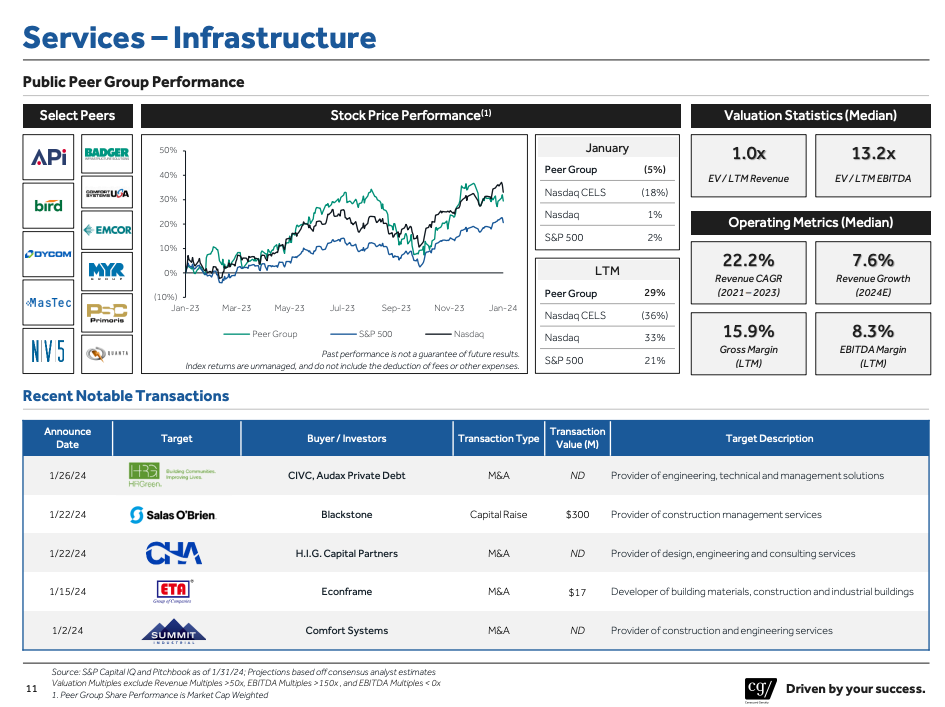

Kyle’s piece inspired me to write about another business model I’ve been thinking about for a while that could grow in importance over the next decade: services. It’s a sector where private equity has done well and where smart firms are playing today. It’s also a model where distribution and knowledge moats can be fortified by rapidly creating and leveraging software to expand margins.

The energy transition is complex. How do I plan for an electric fleet? Do I need to build my own microgrid? How big should my onsite battery storage be? What data do I need to measure my emissions? Where’s the best place to put new transmission and generation?

These questions are highly complicated and customer-specific, while the solutions are opaque. They require the customer to have a high degree of trust in the person solving the problem for them. Software can solve many problems, but human trust isn’t one of them.

Some of the best private equity firms have already leaned heavily into this strategy. Oaktree Capital has a history of rolling up EPC firms. At the same time, Summit Partners and Blackstone have purchased several construction services companies. Other PE firms are rolling up HVAC technicians and electricians.

These investments fit the private equity playbook perfectly. The localized offices have built loyal customer bases within their specific region. Once combined with other firms, they can share back office systems and operations. Finally, they usually have a specialized skill in high demand with short supply.

Like hardware, service businesses have to be capitalized appropriately. No matter how digitally-enabled it may become, investing in a services business can’t be done at a 10-20x NTM revenue multiple. They also need to be profitable much earlier, if not from the beginning, as they are ultimately valued on EBITDA and FCF multiples. But, these constraints don’t preclude the businesses from being good investments, far from it.

Services have also held up well in a rocky market for energy transition stocks. Over the last twelve months, infrastructure services have grown 29%, in line with the Nasdaq, while outperforming the S&P 500 and CLES by wide margins. This surprised me, but it makes a lot of intuitive sense:

The IRA and Build Back Better reward deployment

Global infrastructure is aging or being replaced by better solutions

The revenue growth of these firms is now in line with software after the recent pullbacks

Traditionally, service businesses haven’t received the same level of attention and hype as their hardware and software counterparts. But many enduring service businesses are out there, including in seemingly mundane areas like tree trimming.

The energy transition will create more of them in the next decade, and even if they don’t grab attention, they’ll grab returns for the investors who find the right ones.

Imagine returning 30% a year to your investors for 15 years straight. Now, imagine those returns coming during one of the worst periods to be an investor and doubling the returns of the S&P during that timeframe.

That’s how well Peter Lynch performed as head of Fidelity’s Magellan Fund from the late 1970s to the early 1980s.

One of Peter’s most famous quotes relates to the persistence of finding good ideas. He famously wrote in his book One Up on Wall Street:

“I always thought if you looked at ten companies, you’d find one that’s interesting; if you’d look at 20, you’d find two, or if you look at hundred, you’ll find ten. The person that turns over the most rocks wins the game.”

The mentality seems so simple on the surface, but as we’ve learned simplicity is a strategy. If we see more pitches, we’re more likely to get a few worth swinging at. But, staying in this state of mind sets the foundation for success in multiple ways that aren’t as obvious at first glance.

Early in our investing careers, we have almost no idea what we value as an investor. We have no experience sitting in board rooms or the advantage of seeing 100s of deals. We have no idea what great looks like or what matters to us as capital allocators.

As we turn over more rocks, our mind begins to set reference points for excellence, and our core values as investors start to form. We gain a sense of confidence that is informed by data.

Keeping the turning over rocks mentality throughout diligence pays dividends, too. With this mindset, we’re more patient during our research. Instead of looking for answers to validate our thesis, we continually look for data until we are satisfied with the answer.

It’s easy to get swept away in the momentum of any deal. But, having the data gathering approach over thesis validation is an excellent way to ensure that the momentum slows down until we reach a fitting conclusion.

Finally, and most obviously, in private markets, the ability to turn over the most rocks increases our odds of accessing the best companies.

Unlike public markets, private investing naturally limits the number of shareholders on a cap table. The ability to find and efficiently research opportunities more quickly than others AND to do so in the right quarries increases our surface area of success.

Howard Marks started writing his famous memos by hand in the early 1990’s. For 10 years, he never received one response. He claims nobody even responded to let them know they got the letters. For my younger audience, pre-internet everything was sent by this service known as mail.

The answer I think is that I was writing for myself. Number one, it’s creative, I enjoy the writing process. Number two I thought that the topics were interesting and that I wanted to put them on paper. Number three, writing makes you tighten up your thinking. – Marks on Writing

Why did he do it? Marks has stated he was writing for himself, enjoyed having a creative outlet, and wanted to create a record of his thoughts. The more things change, the more they stay they same, as a lot of writers I read list the very same reasons for writing. It’s also the reason I’ve tried to write more and I think “writing for yourself” is under appreciated.

I was reminded of this by Cal Newports’s recent appearance on Ted Ferris to promote his new book “Slow Productivity”. In this clip, Cal emphasizes that the only thing that matters is loving the craft. Apply it, develop it, hone it, and find meaning in it. My favorite line is “don’t require random people on social media or an attention algorithm suck all of that skill out of you.”

Investing is my favorite craft, it has been for the last 10 years. I found it effortless to finish books on Munger, Marks, Schwarzman, KKR, etc… or spend time thinking about companies and thesis building. Writing brings me the same joy, but I never practiced as much because I let the lack of response suck the life out of me. Don’t do that.

As you can tell, I write a lot about failure, writing, and process. I do so because they are all intricately tied together. We learn from failure and process it to take calculated risks and prevent ourselves from making the same mistake twice. We write to process what we’ve learned both in theory and in practice. We refine our processes and learn to enjoy them because they’re usually all we can control.

Investors leverage many tools to make sense of the world – spreadsheets, pitch decks, expert interviews – but few exercises force us to clarify and tighten up our thinking like writing.